The container market continues to impress with record-breaking rates and ordering never seen before.

Olivia Watkins, Head Cargo Analyst of VesselsValue, an online valuation and data provider, takes us through what has been happening with orders, transactions, values, rates and trade for the first half of 2021 and how these sky-high figures compare to previous years’ activity.

Container Ordering

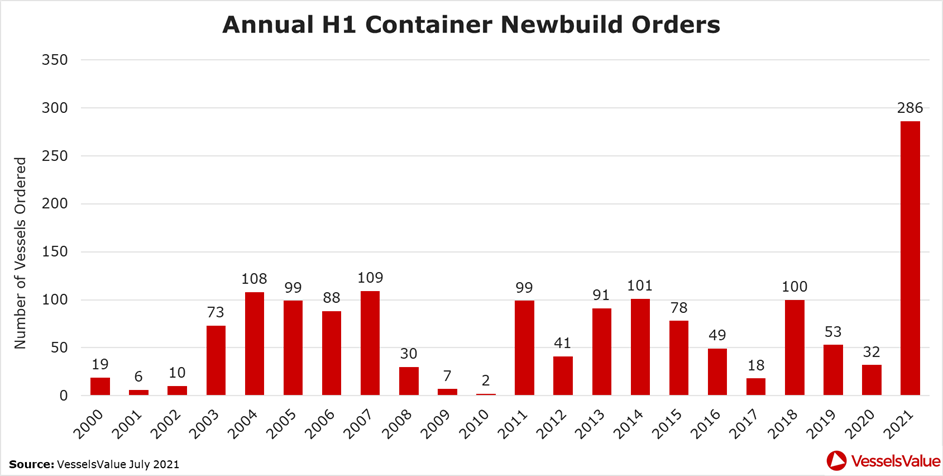

The ordering market for containers is at historic highs. A total of 286 containers were ordered in the first half of 2021. This is up an incredible 790% from H1 2020.

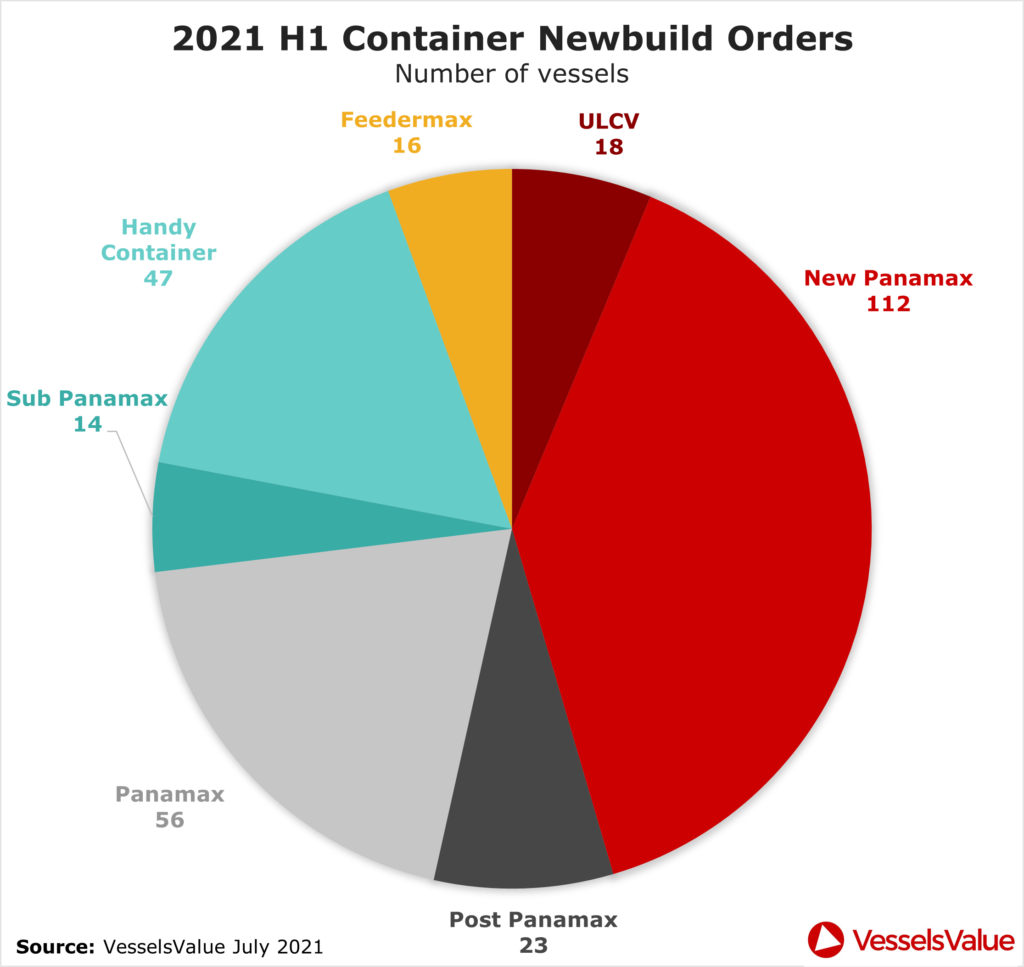

New Panamax container ships, which are typically 13-15,000 DWT, have been at the forefront of the ordering activity. The development of port infrastructure and the ability to fit larger vessels through the Panama Canal has meant this size of vessel is particularly desirable. There are currently 388 New Panamax vessels live on the water at the moment with a further 175 on order across the sector.

Amongst these orders, Seaspan has come in as the top orderer in the first half of 2021, by number of vessels and total value in US$ billion, with all vessels being greater than 12,000TEU which is the New Panamax type.

Evergreen has come in second by total value in US$ billion ordered due to their orderbook comprising of New Panamax and ULCV Containers.

Although Wan Hai Lines is second by number of vessels ordered with the majority of their vessels at around 3,000TEU.

Container Sales

On the contrary to the newbuild orders, we’ve seen a significant increase in activity in the secondhand Panamax container ship market. The number of sales is up 780% for year to date 2021 compared to year to date 2020.

Recent acquisitions where new entrants are paying more than US$100,000 per day for a short-term fixture of between 65-80 days has meant owners like MSC have been buying vessels instead of entering the charter market as it works out more cost-effective.

For example, the vessel Mexico (4,839TEU, February 2002, Hyundai HI) sold for US$50.5 million to MSC at the end of June. The alternative would be to take a vessel on a five-year charter which could cost up to US$70 million.

Another benchmark sale confirmed earlier in June was the ship Kowloon Bay (4,992TEU, July 2004, Hyundai HI) also bought by MSC for US$42.5 million. Kowloon Bay was bought two weeks earlier than the Mexico for US$8 million less.

These sales have shown how the Panamax container ship market is setting new benchmarks each week.

Container Values

With the ever-firming rates across the container sector, we have seen a surge in values. Increased US imports, port congestions and a shortage of capacity are pushing freight rates to record levels on key routes from China to the US and Europe. A secondary outbreak of Covid-19 in Southern China has prompted even more delays and congestion across ports which have tightened supply.

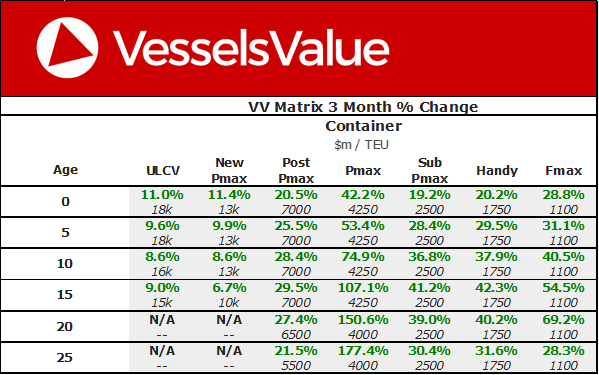

The below figure shows the three-month percentage change in values across the container sector.

As a result of the increased S&P market and rates, the Panamaxes (4,250TEU) have benefitted the most from increased values. For example, 15-year-old 4,250TEU tonnage has more than doubled in value in just three months. At the end of March, a generic 15-year-old Panamax was worth US$20 million, today it is worth US$48 million.

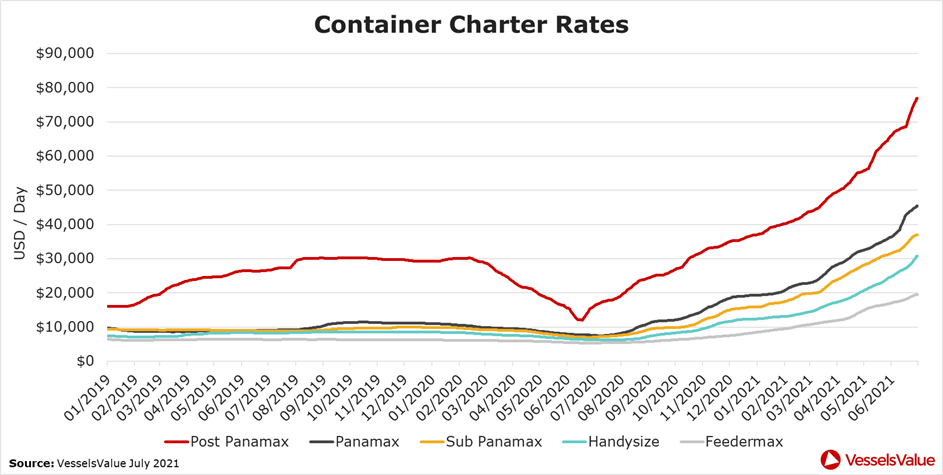

Container Rates

The below figure shows the prolonged increase in charter rates that is impacting the market.

Every single earnings value has more than doubled since the beginning of the year. For example, Panamax container ships were earning US$19,000/day, today they are earning US$45,000/day.

Container Trade

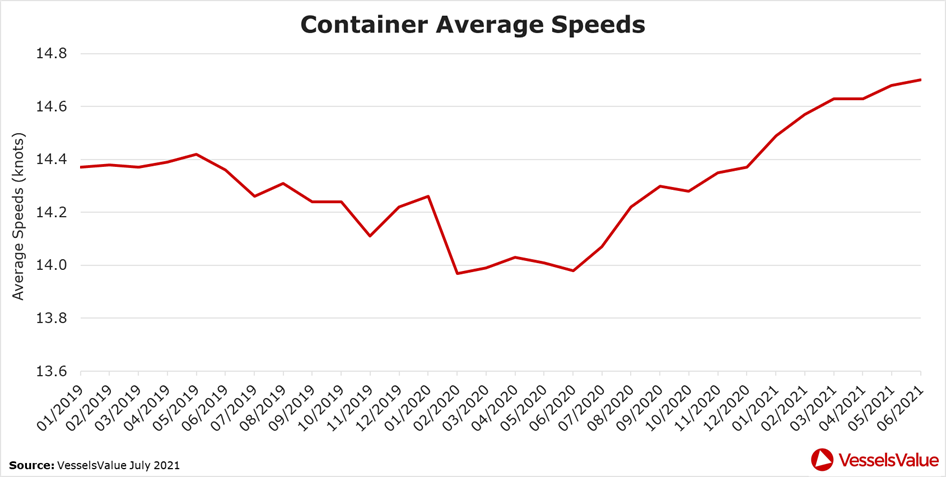

As we surpass the mid-year point of 2021, container vessels’ speeds are continuing to increase, as they have been for the last eight months. The average laden speed across all container ships was 14.70 knots in June, showing a 5.2% YoY growth as well MoM growth of 0.5%. New Panamax vessels take the top spot with speeds of 16.37 knots. These high speeds continue to be supported by favourable market conditions.

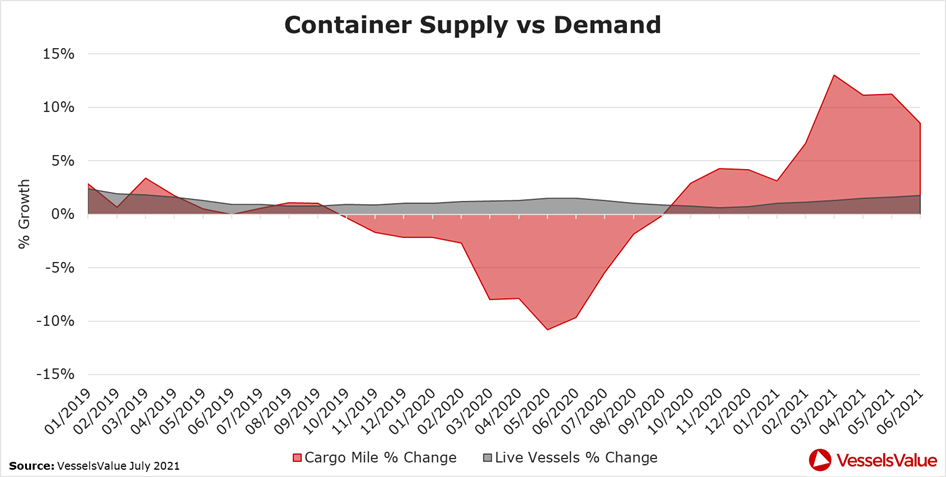

Alongside increasing speeds, cargo miles have been growing through the first half of 2021, with June’s figures at 161.9 billion TEU-NM, almost back to pre-pandemic levels. Fleet growth is set to increase which may disrupt the balance between supply and demand, but for the near future, this balance looks positive for container vessels, as YoY cargo mile growth continues to exceed YoY fleet growth.

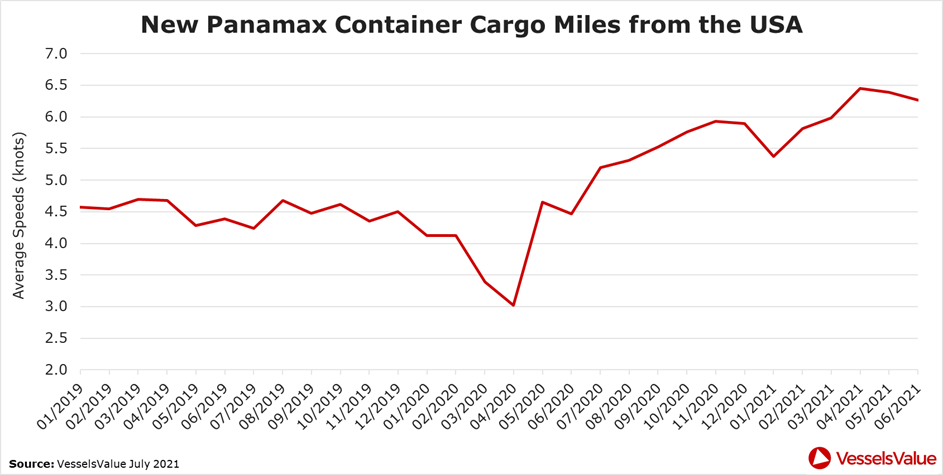

Since the start of 2021, cargo miles from the US rank the highest for New Panamax container vessels, indicating the popularity of US trades for this vessel type, especially in this post-pandemic Covid-19 recovery period.

Appendix

The below table shows VesselsValue’s size breakdown for each container ship category by naming convention, beam and TEU.

VesselsValue data as of July 2021.

Author of the article: Olivia Watkins, Head Cargo Analyst at VesselsValue

Olivia Watkins oversees the Cargo valuation department of the analyst team. Olivia works closely with the Analyst, Research and Development departments of VesselsValue helping to expand the number of vessel types covered and the development and maintenance of new and existing products. Based in London, Olivia is in the middle of market information and intelligence, analysing the S&P, NB and demolition market for Bulkers, Tankers, Containers and Gas. Prior to joining VesselsValue as a Cargo analyst, Olivia attended Southampton University graduating with a BSc in Oceanography.

Disclaimer: The purpose of this article is to provide general information and not to provide advice or guidance in relation to particular circumstances. Views are author’s own